Page 184 - Social Enterprise A New Business Paradigm for Thailand

P. 184

The cooperatives that currently play the most significant economic and social roles are

agricultural cooperatives, savings cooperatives, and credit union cooperatives. Notably, savings

and credit union cooperatives function as financial institutions for grassroots populations who

are unable to access services from commercial banks. The rapid growth of these two types of

cooperatives in recent years has introduced governance risks, with the potential to cause

widespread harm. In 2019, the government responded by enacting the Cooperative Act (No. 3),

B.E. 2562 (2019), which added specific provisions for the regulation and oversight of savings and

credit union cooperatives.

The Cooperative Act established the Cooperative Development Fund, financed through

government budget allocations, to assist, promote, and support the development of cooperatives

and to provide loans for investment and working capital. Oversight is conducted by the

Cooperative Registrar, namely, the Director-General of the Department of Cooperative Promotion,

who is responsible for both promoting and regulating cooperative operations. Cooperative

Inspectors are authorized to examine cooperative activities and financial conditions and submit

their inspection reports to the Cooperative Registrar. Additionally, the Cooperative Auditing

Department serves as the official auditor for cooperatives.

1.1) Tax Obligations of Cooperatives

If a cooperative is established as a legal entity under the Cooperative Act, it is not classified as a

company or legal partnership under Section 39 of the Revenue Code and is therefore exempt from

corporate income tax. Additional tax exemptions are detailed in Table 6.5.

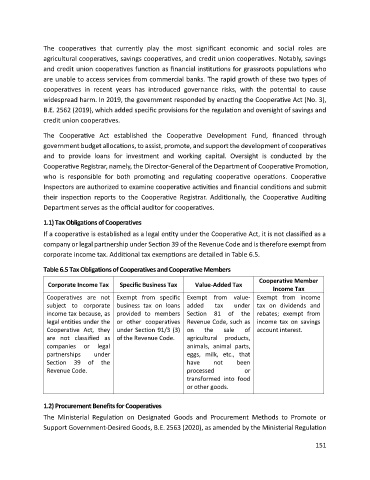

Table 6.5 Tax Obligations of Cooperatives and Cooperative Members

Cooperative Member

Corporate Income Tax Specific Business Tax Value-Added Tax

Income Tax

Cooperatives are not Exempt from specific Exempt from value- Exempt from income

subject to corporate business tax on loans added tax under tax on dividends and

income tax because, as provided to members Section 81 of the rebates; exempt from

legal entities under the or other cooperatives Revenue Code, such as income tax on savings

Cooperative Act, they under Section 91/3 (3) on the sale of account interest.

are not classified as of the Revenue Code. agricultural products,

companies or legal animals, animal parts,

partnerships under eggs, milk, etc., that

Section 39 of the have not been

Revenue Code. processed or

transformed into food

or other goods.

1.2) Procurement Benefits for Cooperatives

The Ministerial Regulation on Designated Goods and Procurement Methods to Promote or

Support Government-Desired Goods, B.E. 2563 (2020), as amended by the Ministerial Regulation

151